The S&P 500 Carry Trade

The world is talking about carry trades, but missing the elephant in the room.

If only there was a book to answer this question.

Turns out, there is.

Tim Lee, Jamie Lee and I published The Rise of Carry in late 2019. We described how and why carry trades have grown to dominate financial markets. The result is that markets, and by extension the global economy, now follow the typical carry trade pattern of small, steady growth punctuated by occasional sudden selloffs. Crashes like what we saw Friday and Monday, like we saw in 2020 and like what we will see again.

It's gratifying to see our ideas become more widely accepted. However, it’s still a smidge frustrating that the carry trade we identified as the most important – the S&P 500 – is still not really recognized as such.

In many way that’s understandable. Thinking of the “stock market” as a carry trade isn’t intuitive. We’re working on a second book where we’ll explain this idea in even more detail. But since the whole world seems to be talking carry trades, I thought I’d use some material from our drafts to discuss it now (and whet your appetite for the next book…)

Below is one of the key passages in the Rise of Carry. The paragraph explains in geeky terms why the S&P 500 is the central global carry trade. I’ll try to de-geek it in next 800 words.

The first line – “S&P 500 volatility has become global volatility” is straightforward.

The S&P 500 is the most visible and heavily traded risk asset in the world. It’s the risk asset at the center of a staggeringly large ecosystem of products that investors around the globe use for speculation and hedging.

Below is a graph I’ve been working on for the new book. WARNING: it’s incomplete1 and I haven’t double-checked all the numbers. Still, it presents a fascinating picture of the annual trading volume associated with the key products linked to the S&P 500. And, yes, all the numbers are in trillions of dollars.

No other equity market comes close to this hyper-liquid ecosystem and this makes the S&P 500 the global epicenter for risk taking and risk hedging. S&P 500 volatility is therefore a proxy for volatility of risk assets everywhere.

Now for the geekier bits.

How does this turn S&P 500 volatility into “generic liquidity risk”? And why would this “define the value of money”?

Being “liquid” means having access to cash. For levered traders that means being able to quickly and cheaply sell what they own in exchange for cash. In The Rise of Carry we document how the world has grown ever more levered over time. Each year more actors need more liquidity. The S&P 500 ecosystem has grown in a symbiotic fashion to provide it.

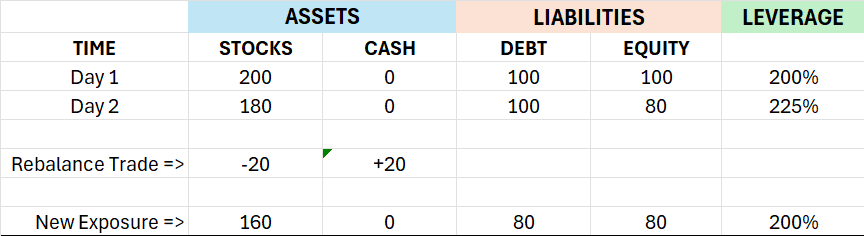

The table below is a very simple stylized example of a levered trader’s need for liquidity. The trader starts Day 1 with $100 and borrows an additional $100 to buy the S&P 500. The first row is the trader’s balance sheet after setting up this levered position. If the S&P 500 falls by 10% on Day 2, leverage goes up to 225%. To return it to 200% the trader needs to sell $20 worth of the market and use the cash – the liquidity they’ve accessed – to pay down their debt. Once they’ve done this they’re back their starting leverage.

Even though it’s very simple, the example highlights three important points.

First, reducing leverage back to target involves trading with the market – selling after it falls.

Second, this trading is not optional. Ok, for small market moves it is – lenders allow leverage to fluctuate around agreed levels. But for big moves the trader must sell to reduce leverage or the person that lent them the money will do it for them.

Third, to supply the liquidity the levered trader needs, some brave soul (or brave algorithm) must take the other side.

I say “brave” because the liquidity supplier buys as the market falls. This exposes them to crashes. For example, imagine you supply liquidity by purchasing the S&P 500 when it’s down 3% on Friday. If it falls another 3% on Monday you’re nursing losses and far less willing to supply yet more liquidity.

It’s easy to see how the non-linear, sharp falls we experienced in the last few days emerge. A big enough jump in volatility causes liquidity supply to fall just as liquidity demand rises. That’s what we mean by volatility “defining the value of money”. When volatility spikes, the value of having cash goes up. And the volatility that matters is S&P 500 volatility because that is a proxy for generic risk asset volatility.

Why should providing this type of liquidity be the “best paying risk in the world”? Because you can’t diversify it away. When S&P 500 volatility spikes there is literally nowhere to hide. Suppliers of liquidity in the S&P 500 ecosystem are taking on the risk of a global crash. That’s why their risk should very well compensated.

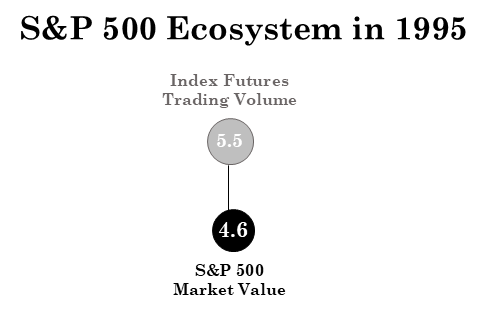

The S&P 500 ecosystem didn’t always work this way. At the start of the carry regime it was more like the stock market we read about in textbooks, where things like earnings and interest rates are the main drivers. Below is my graph of the ecosystem from 1995. Index options did exist but volumes were tiny, so I left them out.

Calling this an “ecosystem” is a stretch. Still, the futures were liquid enough to give the S&P 500 an advantage over other markets in terms of being the preferred location for speculating and hedging. From there growth in the market value of the index, the assets controlled by levered traders and the range of related derivative products reinforced each other. Gradually and steadily the S&P 500 ecosystem became the central risk marketplace it is today.

When volatility rises a reflexive feedback loop develops within this ecosystem. Liquidity providers pull back and that forces liquidity demanders - the levered traders - to sell at lower prices. That in turn pushes prices lower and causes a further diminution in liquidity supply.

Most of the time this doesn’t happen. In fact most of the time there are plenty of liquidity suppliers and their activity helps the market self-stabilize. But when some force, random or fundamental, triggers a big enough jump in volatility, the feedback loop switches to being self-reinforcing and we get a sudden crash.

This is how carry trades work. They make money “when nothing happens”, when volatility is stable or falling. But when something does happen and volatility spikes we get a sudden and very sharp drawdown. That’s exactly the pattern of returns the S&P 500 has adopted as the carry regime has progressed over the last thirty years. And that’s why we say the “absorption of generic liquidity risk must convert the S&P 500 into a giant carry trade”.

This isn’t your grandfather’s S&P 500. It’s the most important carry trade in a world awash with them.

You Might Also Like:

Inflation In The 21st Century Part II: Unintended Consequences

Inflation In The 21st Century Part III: The Dollar's Circular Flow Comes To An End

For instance it doesn’t include over-the-counter structured products. It’s also missing a option-based ETFs, levered ETFs and ETFs listed in other countries.

100 per cent. Well explained. Aside from volatility, all leverage is a “carry trade”. Without FX exposure, leveraged investors borrow at X% to buy assets that they hope will appreciate by more than X%. Then you add in FX risk and it really gets fun. You are betting on stability. And as you say and as we all learned from Long Term Capital, when everyone wants or has to sell everything is correlated.

In lieu of liquidity/maturity mismatches, a strategy if it could have been implemented would have been to borrow long in Yen without margin call risk so as to be able to ride out the storms

Awesome read as always professor! Just out of curiosity, will be new book be called “The fall of carry”? 😄